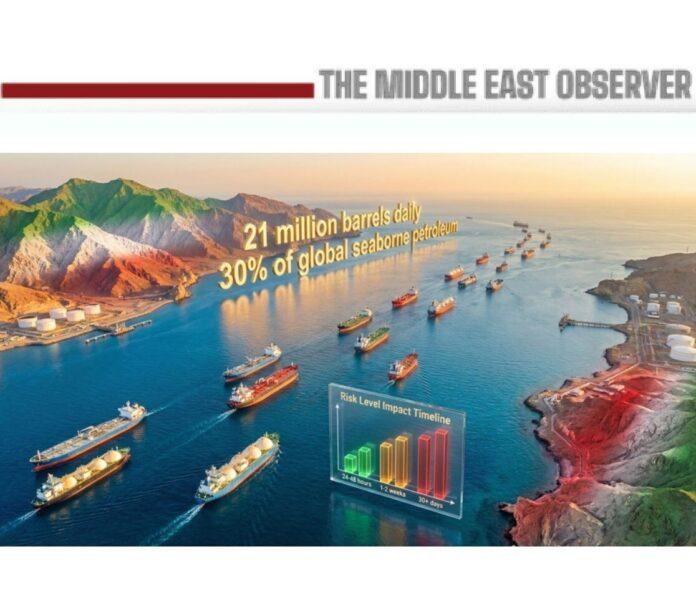

As disruption in the Strait of Hormuz evolves into a structural risk, Gulf energy exporters are diverging between those able to reroute supply and those forced into mitigation. Saudi Arabia and the UAE lead immediate alternatives, while Egypt’s SUMED corridor and emerging land corridors are reshaping regional logistics.

The sustained disruption of the Strait of Hormuz is driving a fundamental reordering of global energy flows, exposing a widening structural divide among Gulf producers between those with alternative export routes and those still dependent on a single maritime chokepoint.

At the forefront of this transition is Saudi Arabia’s East-West pipeline, or Petroline, which extends from the Kingdom’s eastern oil fields to the Red Sea port of Yanbu. With a capacity of up to 7 million barrels per day, the system has enabled Riyadh to rapidly redirect crude exports away from the Gulf, with volumes from Yanbu rising sharply within weeks of disruption. Originally developed in the 1980s following tanker security threats during the Iran–Iraq War, the pipeline now stands as the region’s most advanced and scalable non-Hormuz export solution.

Yanbu is simultaneously evolving from a contingency outlet into a fully integrated industrial and logistics hub. Anchored by major refining complexes and supported by expanding downstream and clean energy investments, the Red Sea corridor is increasingly positioned as a parallel export and industrial platform aligned with Vision 2030.

The United Arab Emirates has deployed a comparable, though more limited, solution through the Habshan–Fujairah pipeline, which transports up to 1.5 million barrels per day of crude to the Gulf of Oman, bypassing the Strait of Hormuz. Fujairah has consequently developed into a critical storage, refining and bunkering hub, reinforcing the UAE’s capacity to maintain export continuity under stress conditions, although parts of its gas and LNG infrastructure remain exposed to Gulf transit routes.

Beyond pipelines and maritime routes, Saudi Arabia is also expanding land-based logistics corridors as part of a broader redundancy strategy. The state railway operator Saudi Arabia Railways has launched a new freight rail service linking the eastern ports of King Abdulaziz Port (Dammam), King Fahd Industrial Port (Jubail), and Jubail Commercial Port to the northern border crossing at Al Haditha. This corridor establishes a direct overland connection to Jordan and onward to northern markets.

The route—spanning more than 1,700 kilometres—cuts transit time by roughly half compared to conventional trucking, with each train capable of carrying over 400 standard containers. Beyond efficiency gains, the corridor enhances supply chain resilience, reduces reliance on road freight, lowers carbon emissions, and strengthens Saudi Arabia’s integration into regional trade networks. While not a substitute for seaborne energy exports, this rail axis represents a critical logistics diversification layer, supporting petrochemicals, refined products, and containerised trade linked to energy value chains.

Beyond Saudi Arabia and the UAE, structural limitations are becoming increasingly evident—and are now translating into operational disruption.

Qatar, the world’s largest exporter of liquefied natural gas, remains heavily reliant on maritime routes through the Strait of Hormuz from its Ras Laffan complex. In response to recent disruptions, the country has declared force majeure on selected LNG cargoes and reduced production levels, reflecting the absence of viable rerouting capacity. While the Dolphin Gas Pipeline provides limited regional export flexibility, it cannot substitute for Qatar’s global LNG supply chain, leaving the country structurally exposed to prolonged transit constraints.

Kuwait faces a comparable challenge in crude exports, lacking direct pipeline access to open waters beyond the Gulf. In recent weeks, Kuwait has reduced output, invoked force majeure on certain cargoes and relied on storage to manage supply imbalances. Although longer-term options include potential overland connectivity to external export nodes such as Oman’s Duqm and Ras Markaz corridor, or integration into regional pipeline systems, no immediate bypass solution is currently available.

Within this evolving landscape, Egypt is reasserting its role as a strategic transit state linking Gulf production to European and Mediterranean markets. The SUMED Pipeline, extending from Ain Sokhna on the Red Sea to Sidi Kerir on the Mediterranean, provides a critical overland bypass to the Suez Canal. With a capacity of approximately 2.5 million barrels per day, the system enables crude to be transferred across Egypt for onward export to Europe, reducing reliance on vulnerable maritime chokepoints.

Complementing this infrastructure, the Suez Canal remains a major artery for refined products and LNG flows, although capacity limitations and geopolitical exposure constrain its ability to fully offset Hormuz-scale disruption. Together, the SUMED–Suez axis forms a central component of an emerging westward energy corridor, particularly for Saudi and Iraqi crude redirected via the Red Sea.

The integration of both Egypt’s transit system and Saudi Arabia’s expanding rail corridors underscores a broader structural shift: the emergence of multi-layered export networks combining pipelines, ports and inland logistics routes. Under a prolonged disruption scenario, this system is likely to expand further, supported by increased investment in storage, refining, transshipment and cross-border connectivity.

Despite these developments, a significant capacity gap remains. The Strait of Hormuz typically facilitates close to one-fifth of global oil consumption, far exceeding the combined capacity of existing alternative routes. Even with Saudi Arabia’s Petroline, the UAE’s Fujairah corridor, Egypt’s SUMED system, and emerging land logistics networks, a substantial share of Gulf exports would remain constrained.

A clearer strategic hierarchy is therefore emerging. Saudi Arabia is best positioned, supported by its pipeline network, Red Sea infrastructure and expanding inland logistics corridors. The UAE follows with a functional, though more limited, bypass via Fujairah. Egypt is increasingly central as a transit enabler bridging Gulf and European markets. Kuwait and Qatar, by contrast, are operating in mitigation mode, relying on production adjustments, storage capacity and contractual flexibility rather than rerouting infrastructure.

The broader implication is that the Gulf’s energy future is no longer defined solely by production capacity, but by route optionality. Infrastructure once regarded as redundant has become central to supply security. Should disruption in the Strait of Hormuz persist, investment is likely to accelerate toward pipelines, ports and integrated corridors—both maritime and inland—that enable producers to access global markets without reliance on a single vulnerable chokepoint.

In this context, the map of global energy logistics is being redrawn—not gradually, but under the pressure of immediate geopolitical necessity—with the development of resilient, multi-modal export networks emerging as a strategic imperative for the region.