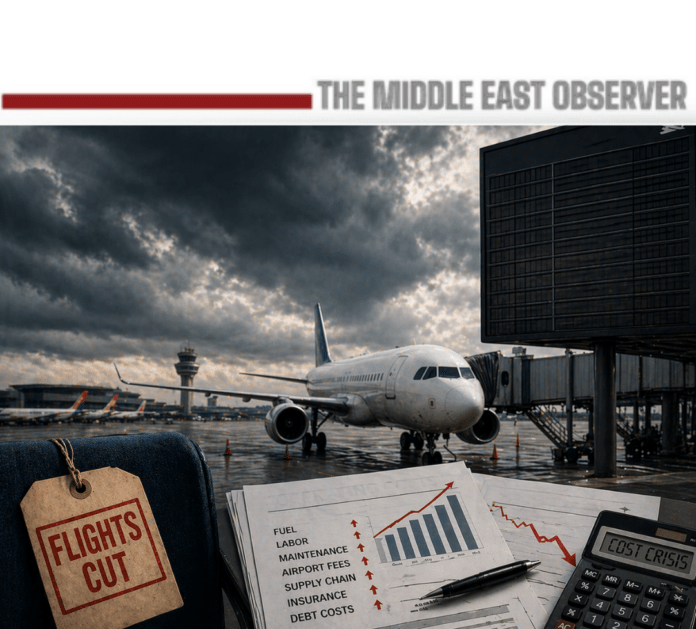

Europe’s aviation sector is facing mounting pressure as rising jet fuel costs—driven by disruptions in the Middle East—force airlines to scale back operations and adjust pricing strategies.

Lufthansa confirmed it will cut around 20,000 European short-haul flights this summer, citing unprofitable routes amid fuel prices that have reportedly doubled since the escalation of regional tensions, according to the BBC. The airline expects to save approximately 40,000 metric tons of fuel, while continuing to review its European network.

The move reflects a broader industry trend. Air France-KLM and Delta Air Lines have reduced selected routes and increased ticket prices, while other carriers are optimizing schedules, consolidating frequencies, and prioritizing long-haul and higher-yield routes to manage rising costs.

The pressure stems from disruptions to fuel supply chains linked to the Strait of Hormuz, a critical artery for global energy flows. The International Energy Agency has warned of tightening jet fuel markets in Europe, prompting the European Union to establish a fuel monitoring mechanism to track supply risks and price volatility.

A key question emerging is whether the jet fuel shortage affects only commercial aviation or extends to military operations. Current assessments indicate that military supply chains remain largely insulated, supported by strategic reserves and prioritized logistics frameworks. However, prolonged disruption could increase procurement costs, even if supply availability remains stable.

Across the sector, restructuring is accelerating. Airlines are reducing short-haul frequencies, deploying larger aircraft on consolidated routes, suspending marginal destinations, and increasing fares—while maintaining long-haul connectivity to protect revenue streams. This reflects a shift toward efficiency and cost control rather than expansion.

The Middle East Observer notes that aviation is entering a structurally higher-cost environment shaped by energy volatility and geopolitical risk, where reduced capacity and higher fares are likely to persist if fuel pressures continue.

In the near term, airlines are expected to deepen capacity cuts, maintain elevated fares, and prioritize long-haul routes, reinforcing this higher-cost operating model.

Over the medium to longer term, a disruption lasting six months or more would drive structural change. Analysis from the International Air Transport Association and the International Energy Agency points to key shifts: diversification of fuel supply chains, expansion of strategic reserves, accelerated adoption of Sustainable Aviation Fuel (SAF), and network restructuring toward fewer, more efficient routes.

In parallel, governments are expected to strengthen energy and logistics resilience through alternative refining capacity and more secure supply routes—marking a transition from cost efficiency to supply security and operational resilience.

Ultimately, if the crisis persists, the aviation sector will move beyond short-term adjustment into structural transformation, with long-term competitiveness increasingly defined by how effectively airlines and governments reduce reliance on volatile fuel supply chains and build more resilient, diversified energy frameworks.